In this blog post, you will learn everything you need to know about the new Corporate Sustainability Reporting Directive (CSRD), the requirements for companies and how sproof sign can help you overcome these challenges.

What is the CSR reporting obligation?

The CSR reporting obligation, or Corporate Social Responsibility reporting obligation, is a legal requirement according to which companies must regularly report on their sustainability activities. These reports cover environmental, social and governance (ESG) aspects and are intended to increase transparency about the non-financial impact of the company. The aim is to provide stakeholders – including investors, customers and the public – with comprehensive information about the company’s sustainability practices and social responsibility.

What does the new sustainability reporting obligation mean for you?

The CSRD will come into force in 2024 and significantly expands the previous Non-Financial Reporting Directive (NFRD). The aim is to standardise and regulate reporting on sustainability issues in order to ensure increased transparency on environmental and social aspects of the company. But what does this mean for your company?

What do you have to report?

Companies must disclose comprehensive information about environmental, social and governance (ESG) aspects. These include environmental concerns (e.g. emissions, energy consumption), social aspects (e.g. working conditions, equality), employee concerns, respect for human rights and the fight against corruption and bribery. These reports must include both qualitative and quantitative data and be both forward-looking and retrospective. In addition, they must cover the entire value chain of your company.

Who is affected?

The CSRD applies to all large companies that meet at least two of the following criteria:

- More than 250 employees

- A balance sheet total of over 20 million euros

- A net turnover of over 40 million euros

This means that many more companies than before will have to disclose their sustainability measures.

When do you need to act?

The new rules will be implemented in three phases:

- from 01 January 2024 for companies already subject to the NFRD (first reporting 2025)

- from 1 January 2025 for large companies that were not previously subject to reporting requirements (first reporting in 2026)

- from 01 January 2026 for listed SMEs (first reporting 2027), with an opt-out option until 2028

Reporting framework: format and standards

With the CSRD, the EU has introduced uniform European reporting standards that companies must use for their sustainability reports. These standards, known as “European Sustainability Reporting Standards” (ESRS), were developed by the European Financial Reporting Advisory Group (EFRAG) and transposed into applicable law by the European Commission.

The first regulations will come into force from 2024 and include twelve standards covering environmental, social and governance issues as well as overarching requirements.

There are simplified reporting standards for small and medium-sized enterprises that will apply from 2026:

- Companies must report according to the principle of double materiality . This means that they must disclose both the impact of their actions on the environment and society as well as the impact of environmental and social changes on their business.

- Reports must be prepared in a digital, machine-readable format and independently audited to ensure compliance with the standards.

In the future, industry-specific reporting standards are also planned to further specify reporting.

The e-signature is an important tool for achieving the Sustainable Development Goals

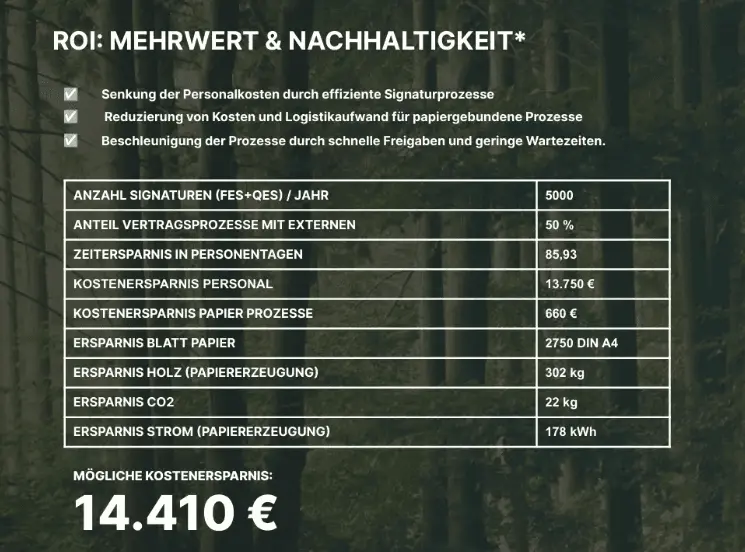

The digitization of business processes is an essential lever for efficiently meeting the requirements of the CSRD. A basic process that should therefore be digitized is the signing of contracts and documents. From the first day of the nationwide introduction of e-signatures, a company can measurably save a large amount of paper-based resources. resources that pollute the environment.

An example: Let’s assume that any company saves (only!) 500 sheets of paper within a certain period of time thanks to the integration of e-signature. This measure already leads to a reduction in consumption of 7.5 kilograms of wood, 130 liters of water and 26.8 kilowatt hours of energy.

The use of digital signatures can therefore be a key to efficiently meeting the requirements of the CSRD and an important step towards more sustainable corporate governance, as well as calculating exactly how many resources have been saved.

Compulsory or freestyle? Is sustainability reporting also worthwhile on other levels!?

The obligation to report on ESG seems annoying to many companies at first. In fact, the effort is also worthwhile for organizations that are not covered by the CSRD or SFDR (Sustainable Finance Disclosure Regulation). After all, making one’s own sustainability transparent is increasingly becoming a competitive advantage:

- Strengthen reputation and brand: Consumers value sustainability. ESG reporting can improve your company’s image and brand, which helps attract new customers and retain existing ones.

- Convincing investors: More and more investors are taking sustainability into account in their decisions. Transparent ESG reporting can make your company more attractive to investors.

- Improve recruiting: Sustainability is a decisive criterion for many job seekers. A good ESG report can help you attract and retain top talent.

- Save resources: By defining and measuring ESG KPIs, companies can save resources in a targeted manner, for example by reducing energy consumption and thus reducing costs.